Who Really Leads AI in 2026

Right now, the AI and “futuristic tech” landscape is dominated by a small set of infrastructure giants (chips and cloud) plus a handful of frontier‑model companies that sit on top of that stack. Together, they capture most of the revenue, valuation and strategic influence in AI.

At the core of current rankings you typically find: NVIDIA as the leading AI‑hardware powerhouse, Microsoft, Amazon and Alphabet (Google) as cloud‑plus‑AI platforms, Apple and Meta as ecosystem and consumer‑data superpowers, and specialized AI labs like OpenAI and Anthropic as model‑centric players.

Rankings and Scale: Who Is on Top

Analyses of “top tech” and “top AI” companies for 2026 consistently highlight a few names at the very top:

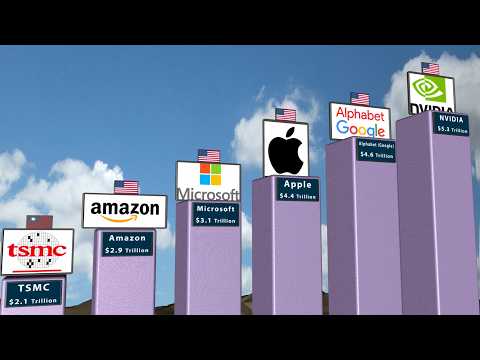

One global overview notes that NVIDIA, Apple, Microsoft, Alphabet (Google) and Amazon “dominate” lists of the world’s top tech firms, with NVIDIA recently becoming the first to hit around a 5‑trillion‑dollar valuation on the back of the AI boom.

A separate 2026 Wall Street Journal–style ranking of “best companies for the future” places NVIDIA at number one, with Alphabet, Microsoft, Meta and Cisco in the top five, emphasizing their AI readiness and ability to shape the next decade.

Social‑media and market‑cap snapshots for early 2026 show NVIDIA leading global tech by market value, followed by Alphabet, Apple, Microsoft and Amazon, with TSMC, Meta, Broadcom, Tesla and Samsung rounding out the extended top 10.

On the more AI‑specific side, curated lists of top AI companies emphasize:

NVIDIA as the dominant AI‑compute supplier, with more than 80% share of high‑end AI accelerator markets and a multi‑trillion‑dollar market cap.

Microsoft, Amazon (AWS) and Google/Alphabet as the most important cloud‑AI platforms, providing managed models and infrastructure to thousands of enterprises.

OpenAI, Anthropic, Google DeepMind, Meta AI and Microsoft as the leading model‑centric companies, with valuations in the tens to hundreds of billions and flagship products like GPT‑5, Claude, Gemini and Llama.

In short: chips (NVIDIA), clouds (Microsoft, Amazon, Google), ecosystems (Apple, Meta) and model labs (OpenAI, Anthropic) together define the current AI hierarchy.

Revenues: Where the AI Money Actually Is

While valuations are eye‑catching, revenue tells you where customers are really spending. Recent industry snapshots provide useful estimates:

A 2026 business breakdown of top AI companies notes that NVIDIA generates more than 130 billion dollars in annual revenue (FY 2025 numbers) largely from AI chips and data‑center hardware, with its market cap around 4.5 trillion at that point—and significantly higher by 2026.

The same source estimates Microsoft at roughly 280 billion dollars in total revenue for FY 2025, with over 42 billion coming specifically from AI‑driven services via Azure and its partnership with OpenAI.

Amazon’s AI strategy is described as running “across industries and client sizes,” with AWS empowering thousands of businesses; Amazon’s overall revenue is cited at more than 280 billion dollars, and separate commentary estimates AWS’s AI‑related cloud revenues at roughly 38 billion annually.

A 2026 LinkedIn‑style analysis of “AI revenue leaders” estimates: NVIDIA at roughly 125–215+ billion in total revenue (with a large share from AI hardware), Microsoft at over 45 billion in direct AI/cloud AI revenue, Amazon at about 38+ billion in AI‑related cloud revenue, Alphabet at roughly 30+ billion in AI/cloud revenue, and OpenAI targeting 12–30 billion in ARR depending on scenario.

Dedicated AI‑lab valuations also stand out:

A 2026 market‑overview of “best AI companies” cites OpenAI at around a 157‑billion‑dollar valuation with products like ChatGPT, GPT‑5 and Sora; Anthropic above 60 billion with Claude; and Google DeepMind, Meta AI and Microsoft as key model and infrastructure leaders.

These numbers show that most AI revenue still flows through the infrastructure layer (chips and cloud), while standalone model companies are growing quickly but from smaller bases.

Visions: What These Companies Are Trying to Build

NVIDIA – AI as a Utility

NVIDIA’s vision, as described in 2026 deep‑dive analyses, is to be the “picks and shovels” of AI:

It aims to supply everything from data‑center accelerators and networking to software (CUDA, libraries) and turnkey AI supercomputers that governments and corporations can use as national or sovereign AI infrastructure.

Strategic commentary highlights expansion into robotics, automotive platforms, and edge AI devices, wrapping hardware with software and cloud partnerships to become a full AI stack provider, not just a chip vendor.

The positive side of this vision is faster AI adoption in sectors like healthcare, logistics and energy; the critical side is deep dependence on one vendor and the energy footprint of massive GPU clusters.

Microsoft – AI Embedded in Every Workflow

Microsoft’s vision—often summarized as “AI copilots everywhere”—is to embed intelligent assistants into every layer of its stack:

Office, Teams, Dynamics, Windows, GitHub and Azure AI are all being infused with copilots that help write, code, analyze, summarize and coordinate.

Its revenue strategy blends subscriptions and usage‑based pricing, aiming to make AI a standard part of workplace tools rather than a separate product.

Positively, this can raise productivity and lower the barrier to sophisticated analytics for millions of workers and public‑sector employees. Negatively, it intensifies concerns about workplace surveillance, vendor lock‑in and the concentration of AI norms (e.g., what models consider “acceptable”) in a single corporate ecosystem.

Amazon – AI as the Operating System of Commerce and Cloud

Amazon’s vision is to weave AI into every layer of commerce and infrastructure:

On the cloud side, AWS wants to be the neutral platform where customers can choose different AI models and build custom solutions, while Amazon Bedrock and related services provide managed, scalable AI foundations.

On the retail and logistics side, AI optimizes inventory, route planning, pricing and recommendations, aiming for near‑frictionless fulfillment and personalization.

This supports small businesses, reduces transaction costs and can enable more efficient resource use—but it also raises ongoing issues around worker conditions in warehouses, dominance over third‑party sellers and environmental impact.

Alphabet / Google – AI‑First Interfaces to the World’s Information

Alphabet’s AI vision centers on integrating powerful models into all user touchpoints:

Search becomes conversational and multimodal; Gemini‑class models sit behind Gmail, Docs, Android, YouTube and Cloud, turning Google into a unified AI platform.

DeepMind and Google Cloud push into scientific discovery (e.g., protein folding, materials) and domain‑specific AI solutions.

The upside is richer, more context‑aware access to information and tools across languages and devices. The downside is further concentration of power over knowledge discovery, advertising and political communication.

OpenAI, Anthropic and Other Labs – Frontier Agents and General Intelligence

Frontier AI labs pursue more ambitious goals:

OpenAI is described as targeting 12–30 billion dollars in revenue while building increasingly capable multimodal and “agentic” models that can handle complex workflows.

Anthropic emphasizes safety and reliability, pushing for constitutional AI and more steerable systems while racing to scale capabilities and revenues.

They promise powerful assistants and agents that can manage entire projects or business processes—but also intensify safety debates around misuse, alignment, and concentration of general‑purpose capabilities in a few private entities.

Positive Societal Contributions

Across all these players, several genuine contributions stand out in current analyses:

Productivity and new tools: AI copilots, generative tools and model APIs let individuals and small organizations access capabilities that used to require large teams—coding, design, data analysis, translation—improving efficiency and lowering barriers to entrepreneurship.

Innovation in health, science and climate: GPU‑accelerated models are used for drug discovery, medical imaging, climate modeling and energy optimization, potentially shortening development cycles and improving decision quality in high‑stakes domains.

Global access to information and services: Search, maps, cloud collaboration and AI‑powered translation make knowledge, education and remote work more accessible across borders, including in lower‑income regions.

If paired with good policy and governance, these advances can support real progress in healthcare, education, climate mitigation and inclusive economic growth.

Critical Concerns: Power, Labor and Democracy

At the same time, critical commentary and human‑rights analyses warn that these same companies create serious structural risks:

Concentration of infrastructure power: A small number of firms now control the most advanced chips, clouds and models, making it hard for competitors—and even governments—to operate independently.

Labor disruption and inequality: As AI spreads through HR, finance and operations, workers fear a “tsunami” of automation, and without strong reskilling and safety nets, job displacement could widen inequality even if productivity rises.

Privacy, manipulation and democratic impact: Big Tech’s data practices and AI‑driven recommendation systems have been linked to privacy erosion, algorithmic discrimination, mental‑health impacts and the undermining of democratic processes, prompting calls for tighter regulation and, in some cases, structural remedies.

In 2026, responsible AI is moving from a slogan to a regulatory expectation, and the largest AI and tech firms are at the center of that shift.

Professional Perspective: How to Read Rankings, Revenues and Visions

Looking at “Biggest AI and Futuristic Tech Companies Right Now,” three practical points matter more than any single ranking:

Rankings tell you who controls the infrastructure and user interfaces; in 2026, that is overwhelmingly NVIDIA, Microsoft, Amazon, Alphabet, Apple, Meta and a few frontier labs.

Revenues show that most money is still in chips and cloud, with model companies rapidly growing but still smaller; this shapes where bargaining power and pricing control sit in the stack.

Visions explain how these firms intend to use that position—whether to build open ecosystems that share value widely, or tightly controlled platforms that maximize extraction and lock‑in.

For businesses, regulators and society, the challenge is not simply to identify who is “biggest” or “most futuristic,” but to ensure that these titans’ visions are aligned with long‑term social goals: fair competition, meaningful work, robust privacy, and democratic resilience—not just ever larger data centers and valuations.